SiC now walking the EV/HEV red carpet

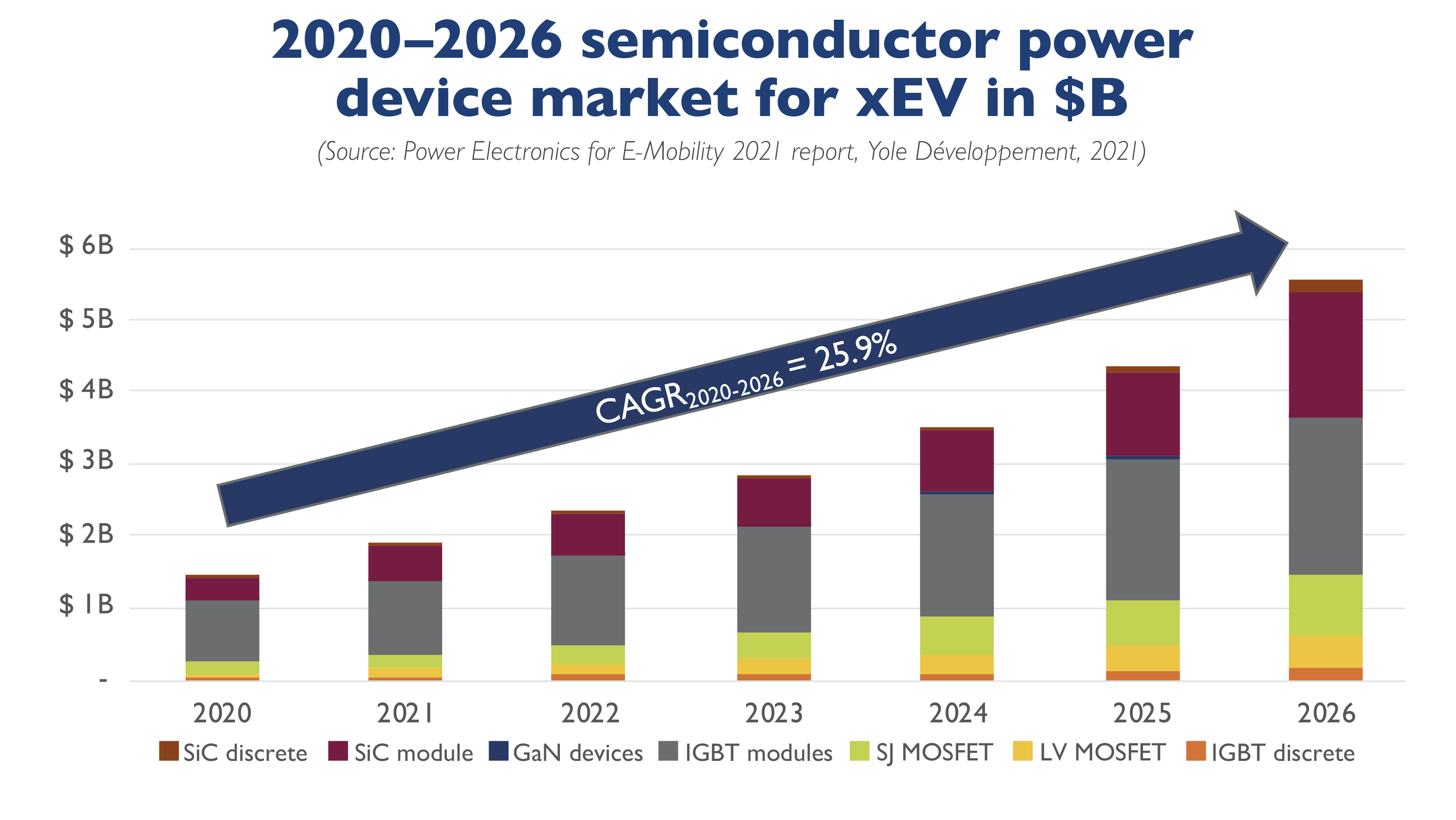

Power semiconductor market will triple from 2020 to 2026, driven by a technology battle between IGBT and SiC modules, says Yole

According to Yole Développement the main power inverter market is expected to reach $19.5 billion by 2026, representing 67 percent of the total EV/HEV converter market, with a CAGR of 26.9 percent. Meanwhile, the total power semiconductor market is expected to triple from 2020 to 2026, driven by a major technology battle between IGBT and SiC modules.

SiC modules are presently still about three times the cost of a 650V IGBT module, but this difference will shrink when larger volumes are produced, with the transition to 8-inch wafers, and with the penetration of 1,200V devices for higher battery voltages.

Yoles Power Electronics for E-Mobility 2021 report provides an overview of the main global drivers for vehicle electrification as well as drivers for each vehicle electrification approach. Il also analyses the changes in business models.

Yole’s team says that the EV/HEV supply chain continues to be impacted by the increased demand and technology trends. Although the leading semiconductor manufacturers for EV/HEV remain the same as for other power applications. It includes Infineon Technologies, STMicroelectronics, Hitachi, Mitsubishi Electric, ON Semiconductor. Other companies, Tier 1s, OEMs, power semiconductor manufacturers, and pure module newcomers, are now offering power modules for EV/HEV. A similar situation occurs with the battery design and manufacturing, where OEMs such as Tesla and GM are further trying to control their supply chains.

According to Milan Rosina, principal analyst, power electronics and batteries at Yole: “Competition at OEM level has also opened two main fronts: on the one hand, there are the traditional OEMs with established markets and known brands that are transforming their business towards electric vehicles. On the other hand, pure EV OEMs are popping up in the different regions of the world (such as NIO, Rivian, Rimac, Xpeng, and Hozon), some of which are rapidly increasing their volumes year after year (lead by Tesla)”.

The new car models being launched often offer better performance/cost ratio, and this has led to a continuous reshaping of the top 10 vehicle sales.

SiC is now walking the EV/HEV red carpet. Over the last couple of years (and especially since Tesla introduced SiC in their Model 3 main inverter), there has been much noise around SiC adoption in EV/HEV. But not all converters or all types of electrification are suitable for this expensive material. Without a doubt, BEV is the winner due to the requirements of a long driving range and fast charging time (km driven by charge time).

Therefore, the increased cost of the converter is repaid, as the efficiency of the converter will improve, allowing battery savings. It is no surprise then that the use of SiC in the main inverter has become a common goal for the leading OEMs, with players such as Daimler and Hyundai soon including it in their main inverters. Who will be next?

Today, there is already a good portfolio of SiC devices with SiC dies coming from Infineon Technologies, Cree (Wolfspeed), and STMicroelectronics. Many semiconductor players are targeting SiC modules for EV applications, and the SiC module market is expected to reach 32 percent of the total EV/HEV semiconductor market by 2026.